Awards and Accomplishment

Innovation Star Named "GCC Company of the Year 2026 for AML Services"

Innovation Star is honored to be named the "GCC Company of the Year 2026 for AML Services." This recognition underscores our continued dedication to delivering cutting-edge anti-money laundering solutions, strengthening financial integrity, and supporting organizations across the region with robust compliance frameworks.

Innovation Star Named "GCC Company of the Year 2026 for Financial Services"

Innovation Star is proud to receive the "GCC Company of the Year 2026 for Financial Services." This award highlights our commitment to innovation, client-centric solutions, and excellence in delivering comprehensive financial services that empower businesses to operate with confidence and compliance.

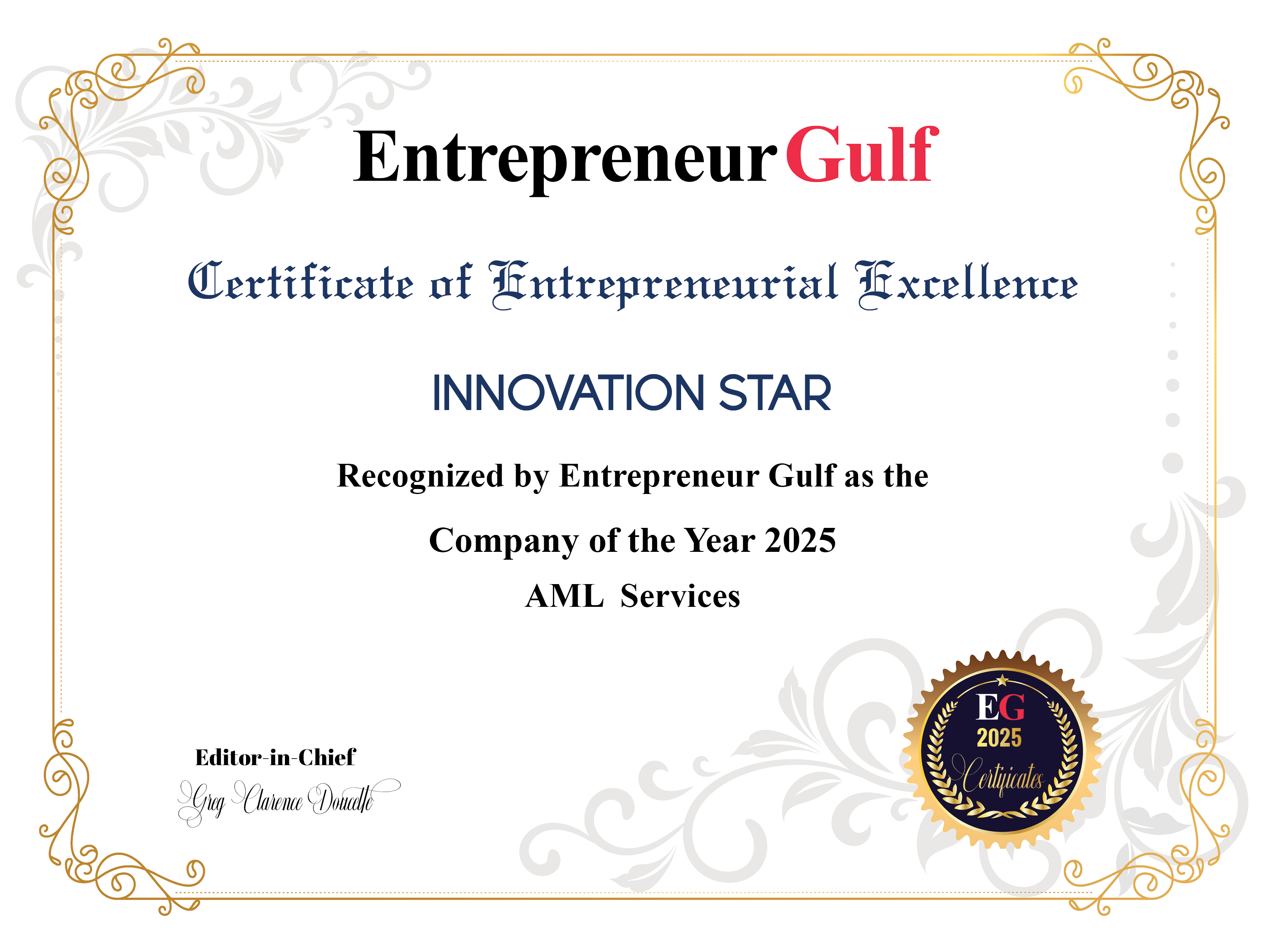

Innovation Star Named "Company of the Year 2025 in AML Services" by Entrepreneur Gulf

Innovation Star is proud to be recognized as the "Company of the Year 2025 in AML Services" by Entrepreneur Gulf. This prestigious award reflects our unwavering commitment to excellence, innovation, and leadership in financial compliance and anti-money laundering (AML).

*Innovation Star Certified as a Great Place To Work® 2025

*Certified for building a trusted, supportive, and high-performing workplace

We are equally proud to share that Innovation Star has been officially certified as a Great Place To Work®. This global recognition highlights the trust, pride, and engagement of our employees, affirming that our success is built on a foundation of not only cutting-edge compliance solutions but also a thriving, supportive, and people-first workplace culture.

Innovation Star Delivers Globally Recognized CPD-Accredited Learning

In line with our dedication to raising industry standards, our AML/CFT/TFS Training for DNFBPs has been CPD-accredited to ensure professionals gain the knowledge and expertise needed to navigate the complexities of Anti-Money Laundering (AML), Countering the Financing of Terrorism (CFT), and Targeted Financial Sanctions (TFS). Furthermore, our CEO and owner, Mr. Pedro Ferreira, has been successfully assessed and awarded Official CPD Standards Office Accreditation, making him an Accredited Provider. This allows our learners to earn internationally recognized CPD hours and certificates through our training programs.

These accomplishments reflect more than recognition—they symbolize our commitment to delivering world-class compliance services, empowering professionals through education, and cultivating a workplace where people thrive. At Innovation Star, we are proud to serve our clients, support our employees, and shape the future of compliance with integrity and innovation.

about section

about section

.png)

.png)